If you are experiencing difficulty managing your student loans, there are federal programs that may offer alternative repayment or relief options based on your eligibility. Allied Enrollment Centers assists with reviewing your situation and preparing the required documentation for submission to your loan servicer in accordance with federal program guidelines. All approvals, payment amounts, and program outcomes are determined by your loan servicer under federal guidelines.

Federal student loan forgiveness programs may be available to certain borrowers based on their loan type, repayment history, employment, and other eligibility factors. These programs are designed to provide potential relief, but not all borrowers will qualify, and outcomes vary depending on individual circumstances and federal guidelines.

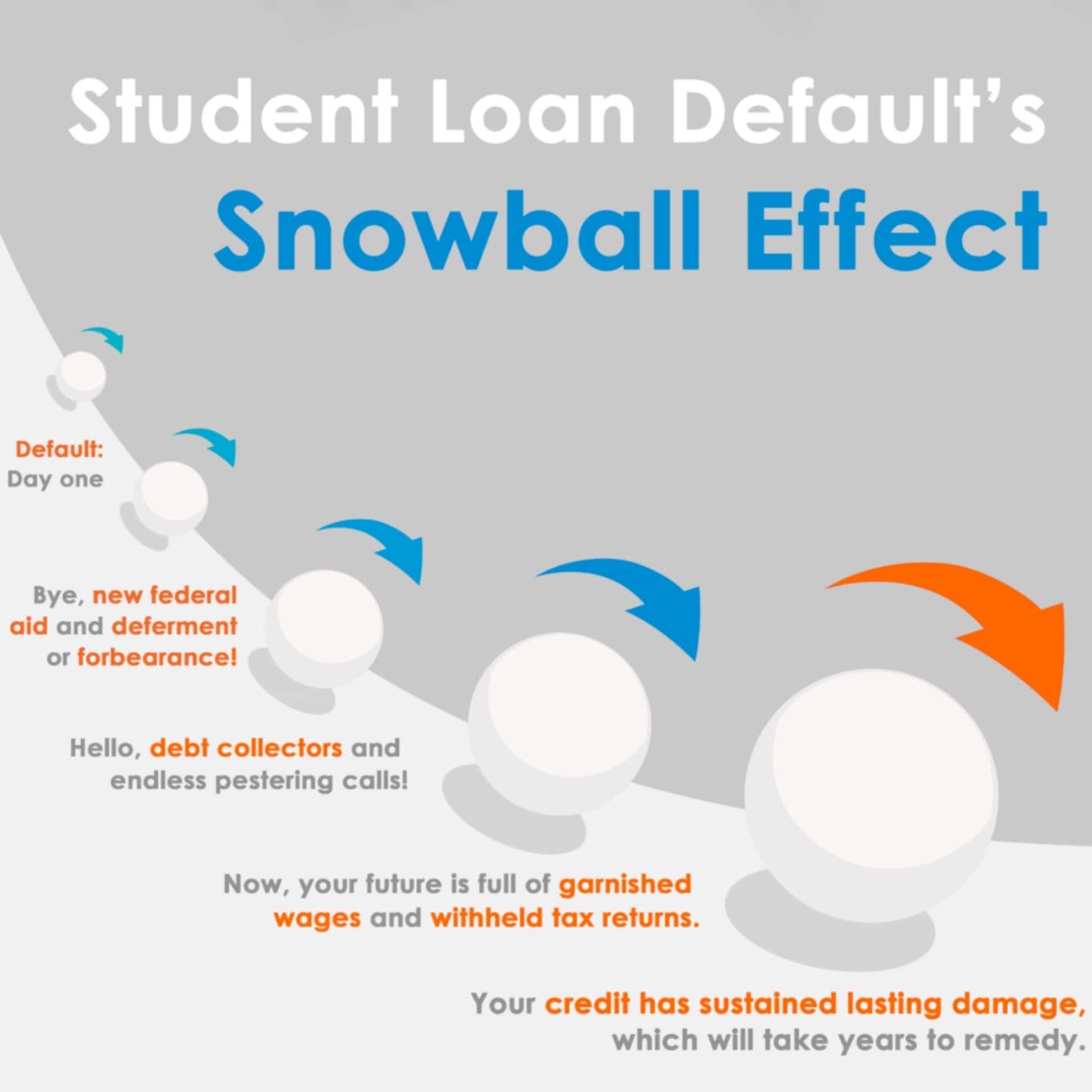

In some cases, borrowers with delinquent or defaulted loans may still have options available, including programs designed to help bring loans back into good standing.

Understanding your student loans starts with a clear picture of your current situation. Loan balances, interest rates, repayment status, and eligibility for federal programs can all impact your available options and long-term costs.

A structured review of your loans can help identify repayment strategies that align with your financial situation, including options that may adjust payments or simplify repayment depending on eligibility.

Loan consolidation is a federal program that allows eligible borrowers to combine multiple federal student loans into a single loan with one monthly payment. This may simplify repayment and can provide access to certain repayment plans depending on eligibility.

In some cases, consolidation may also be used as a step toward qualifying for specific federal programs. However, it may not be the right option for every borrower, and it is important to understand how consolidation may affect loan terms, interest, and repayment timelines.

Federal repayment programs are designed to provide borrowers with flexible options based on their income, family size, and loan details. Depending on eligibility, some programs may adjust monthly payment amounts or extend repayment timelines.

These programs, including income-driven repayment (IDR) plans, are intended to help borrowers manage their payments in a way that aligns with their financial situation over time.